Bitcoin vs Money Supply: 1Q 2023 Update

Executive Summary

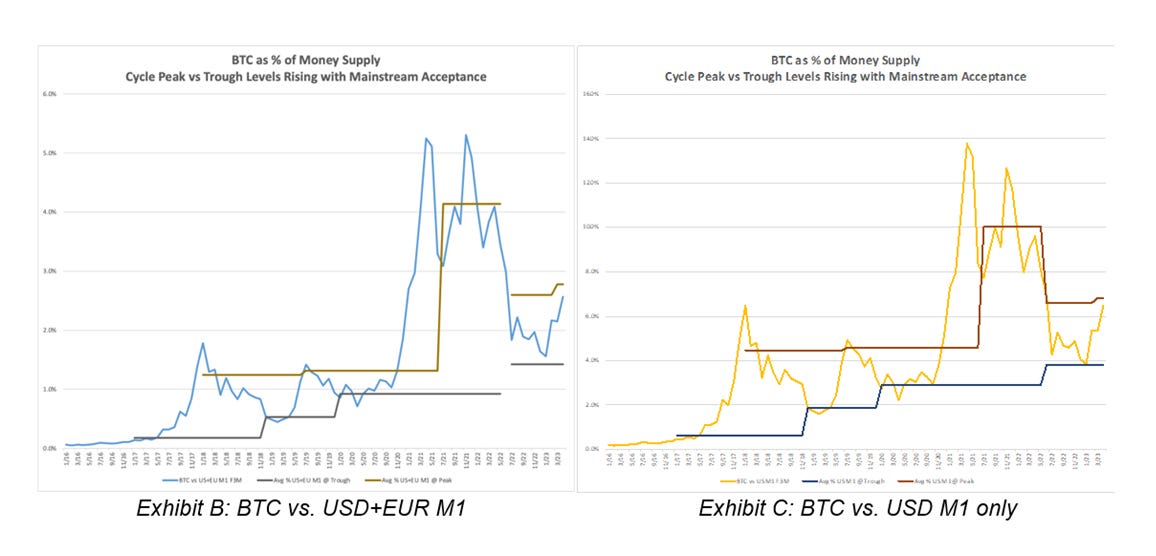

We are refreshing our medium-term view for Bitcoin, which we last published back in August 2022. We employ our proprietary Fiat Money Supply framework (FMS-F) to assess the valuation range and medium direction for Bitcoin, and our key conclusions for now are:

Despite the recent uptick in fiat money supply, this cycle is not yet over due to persistently high inflation-- BUT the 6-month outlook for fiat money supply is uncertain due to the current US bank stress and the recent utilization of the new BTFP (Bank Term Funding Program), which we view as a disguised form of quantitative easing (QE).

With BTC trading at the US$28k level, the risk reward is not very favorable unless more bank runs occur—thus requiring more central bank money printing plus a flight to safety in BTC. Unfortunately, we do not have great visibility regarding this for now, and BTC’s recent rally already captures some of this stealth QE (see Exhibit D).

For now, we slightly adjust our valuation range from the previous 1.4%-2.6% of fiat money supply to 1.4% trough (no change) and 2.8% peak (implying $29.8k upside) for the next 3-6 months.

Yet, within the cryptocurrency market, particularly among large cap tokens, BTC stands out as a safe haven during times of risk aversion. We believe its “digital gold” narrative is finally starting to take hold. This increase in BTC adoption as a store of value is our basis for increasing the upside target. As such, we would overweight BTC relative to other large cap cryptocurrencies.

To access the complete write-up of this research report by GSG, please click on “Bitcoin vs Money Supply: 1Q 2023 Update”.